State of The Markets

Stocks Mixed As The Dollar Rally Continued

STATE OF THE MARKETS

Stocks mixed as the Dollar rally continued. US stocks closed mixed on Wednesday after mixed earnings reports while the Dollar continued to rally past the 103.50 handle as cash demand continued to build amid expected Fed’s 50bps hike in May. Dow (+0.19%) and S&P (+0.21%) eked minor gains while Nasdaq (-0.01%) and Russell (-0.34%) closed in the red. Demand for bonds was muted, sending yields higher with the 10Y benchmark rising back to 2.83% as inversion with the 7Y (2.85%) maturity continues.

In the commodities market, despite Dollar strength, crude was well bid and resilient to close unchanged around $101.50/bl while gold continued its free fall to break below the $1,880/oz barrier. Elsewhere, iron ore pulled back to deeper support as investors weighed the impact of diminishing global growth. The commodity settled lower, around $151.60/tn as New York closed.

In the FX space, King Dollar trumped across all horizons alongside its neighbor Loonie. Demand for safe haven Yen remained in the medium term while short term traders were seen quick in selling the strength following the long term trend. Kiwi and King Dollar were synching across horizons, sending signals that the turnaround is near.

On Thursday, markets continue to look for progress after Russia shut its gas to Poland and Bulgaria, while waiting for earnings reports from Amazon (AMZN), lntel (INTC), McDonalds (MCD), Merck (MRK), Apple (AAPL), Mastercard (MA) and Caterpillar (CAT) as well as the latest US jobless claims, GDP and Fed’s balance sheet to assess the health of the US economy.

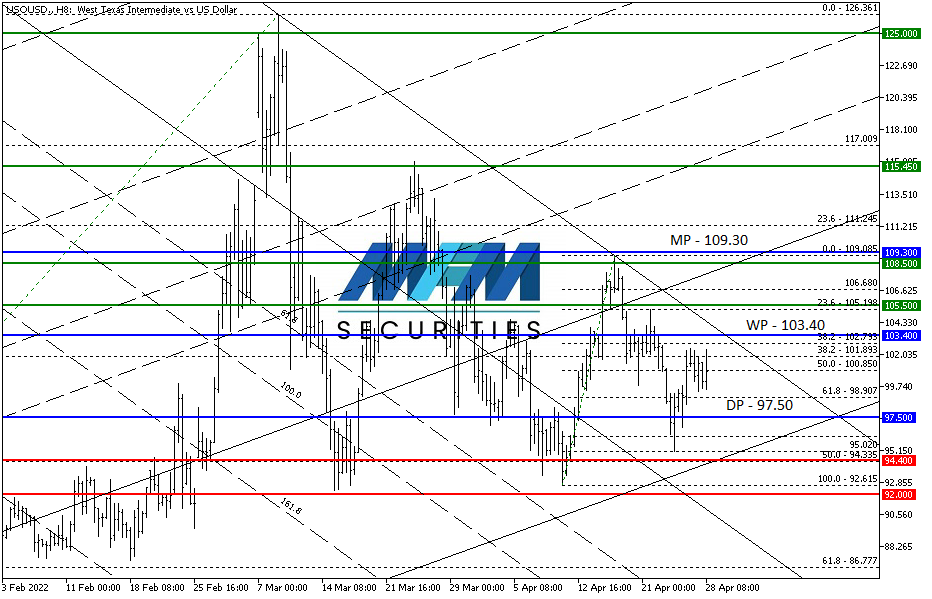

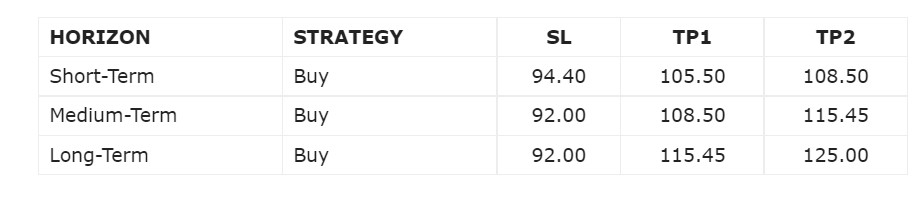

OUR PICK – Crude Oil

Demand outgrow supply and the risk of EU ban. This week has seen strong bids to keep crude oil above $100/bl and we believe it’s the algo that is keeping price elevated despite the US and EIA members SPR release. Research pointed to a quick price escalation if the EU fully banned Russian crude which could see Brent to $185/bl and crude to $128/bl. At this point, the market is waiting and we would cut losses if the price closed below $92.50/bl on the weekly. Short term risk remains, however, that price could test below $97.50/bl in the event of inventories increased.

Risk Disclaimer:

This article is for general information purpose only. It is not an investment advice or a solicitation to buy or sell any securities/oz. Opinions expressed are of the authors and not necessarily of MFM Securities Limited or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

More articles on State of The Markets

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

US New-home Sales Rebound in November After Storm-stricken Month

2

CEO Morning Brief

Orders for US Business Equipment Rise by Most in Over a Year

3

CEO Morning Brief

4

CEO Morning Brief

Google to Fight Japan’s Claims That It Hobbles Rivals in Search

5

CEO Morning Brief

Musk Makes ‘overstaffed’ US Fed Target in Quest for Efficiency

#

Stock

Score

Daily Stocks

Stock

Last

Change

Volume

Stock

Last

Change

Volume

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....